Get Ready for

Nacha Compliance

Trustmi helps you meet Nacha's new ACH fraud monitoring requirements with continuous risk monitoring, account verification, and audit-ready controls.

Risk Assessment

Nacha named the fraud.

Now you’re required to stop It.

For years, companies have lost money to payment requests that looked legitimate, were approved internally, and still turned out to be fraud.

Nacha now calls this false pretenses: payments induced through deception.

Under the 2026 rule changes, organizations are expected to detect and prevent it. Failure can lead to fines, enforcement actions, and loss of ACH privileges.

Why Current Controls Fall Short of What Nacha Requires

For many organizations, bank account validation is the last line of defense. But false pretenses use accounts that can pass those checks.

In reality, an account validation just confirms an account is real, active, and able to receive funds—not that the payment should go there. In fact, 90% of bank accounts used in B2B payment fraud are bank-approved accounts that can pass standard validation checks.

Many fraud controls are designed to catch risk at the moment a payment is created or released. But false pretenses usually happen earlier, before any payment file exists.

Most B2B payment fraud attacks start in email, and 92% involve the impersonation of executives or vendors. By the time the ACH entry is sent, the request may already be approved in workflow and queued for payment.

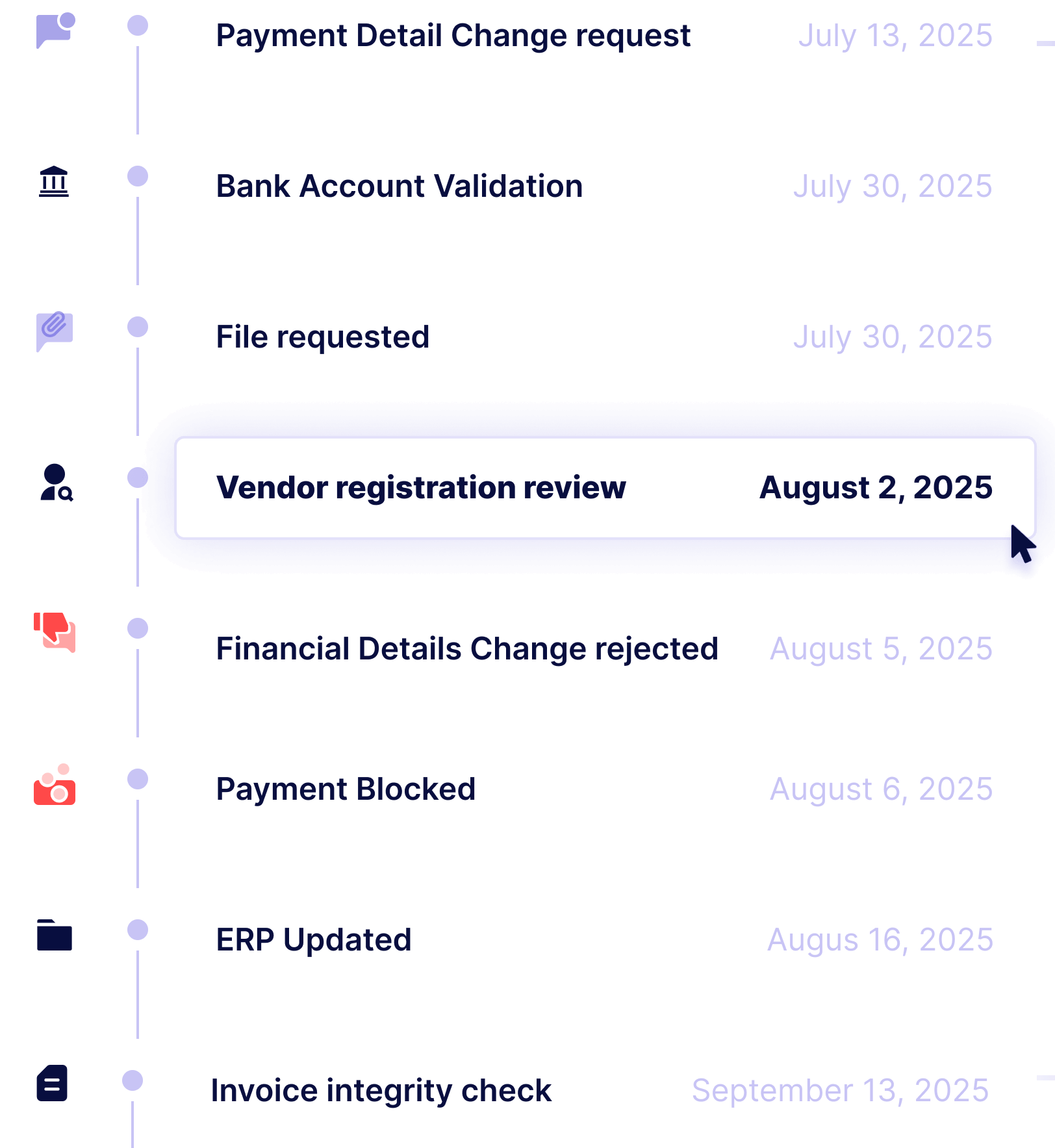

AP teams often rely on verbal confirmations, email threads, and spreadsheet logs to verify payment changes and document approvals.

This manual and fragmented process makes it difficult to satisfy Nacha’s new requirement that procedures be reasonably intended to identify fraudulent entries.

What It Takes to Protect Every ACH Payment

Go Beyond Bank Validation

Stop False Pretenses

Stay Audit-ready

How Trustmi Powers Nacha Compliance

Cross-System Intelligence

Continuous Behavioral AI Fraud Detection

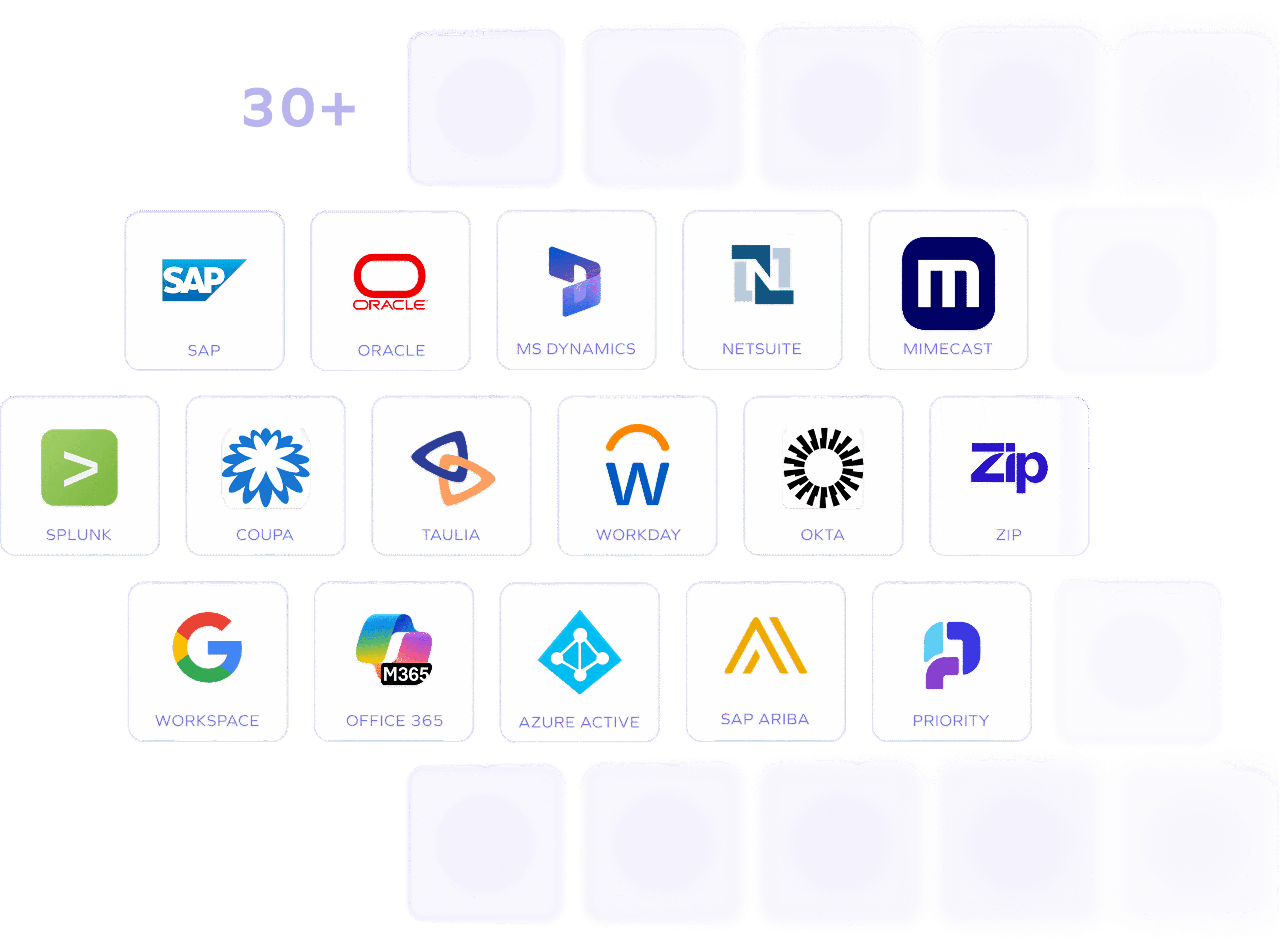

Workflow-Ready Integrations

Proven Across the Trustmi Platform

$1B+ Fraud Prevented

Prevention, not reimbursement.

$240B+ Protected

Trusted with enterprise volume.

90% Less Manual Review

Fewer alerts, faster approvals.

Trustmi is a Preferred Nacha Partner

FAQs

Nacha’s 2026 amendments require all non-consumer Originators, Third-Party Senders, and Third-Party Service Providers to establish documented, risk-based processes for identifying ACH entries that are unauthorized or authorized under False Pretenses. Phase 1 took effect March 20, 2026 for organizations with 6 million or more ACH entries. Phase 2 expands this requirement to all remaining participants effective June 22, 2026.

The previous rules required a vague “commercially reasonable fraudulent transaction detection system” for a limited subset of debit transactions. And this was primarily WEB debits. The 2026 rules extend requirements to ACH credits. It also introduces False Pretenses as a defined fraud category that organizations must actively monitor for.

Account validation does not detect whether a payment request was genuine. False Pretenses fraud specifically targets the space between those two things. An attacker who has compromised a vendor’s email, changed their banking details, and induced an authorized payment has passed every validation check.

No, Nacha compliance doesn’t guarantee complete protection from payment fraud. That’s because compliance is a baseline set of rules, not a security solution. Meeting Nacha’s requirements ensures you follow standardized, risk-based processes, but those checks can still miss sophisticated, socially engineered attacks.

Trustmi goes beyond the checkbox, using Behavioral AI to detect and stop hidden fraud across your entire payment ecosystem before it’s submitted to the ACH network.

Trustmi works alongside existing controls including ACH blocks, filters, and bank-side validation tools. Those controls address unauthorized external debits. Trustmi also addresses the fraud that passes those controls cleanly because it travels inside the authorized payment process.

Nacha compliance under the 2026 rules is not solely a finance or IT concern. It requires coordination across accounts payable, treasury, compliance, and information security. Trustmi connects all of these functions through a single platform, giving each team the visibility they need without requiring manual coordination across systems.

Deploying Trustmi’s Nacha compliance solution is fast, because it connects to your existing systems through ready-made integrations for major ERP platforms, business applications, and payment systems. It plugs in through secure APIs with no changes to your established finance workflows, so your team keeps processing ACH transactions exactly as they do today while Trustmi monitors for fraud continuously in the background.

Trusted by Finance and Security Leaders

“Trustmi provided transparency into our payment process to see where cyberattacks and errors were happening and full protection without changing our workflow."

“Like many businesses today, we’ve experienced cyber attacks on our payment process, but we didn’t realize the extent to which we were at risk until we evaluated Trustmi. Now we’re confident we’ll be able to avoid future attacks with their platform.”

“Trustmi’s platform is an important tool for our team. Their Payment Flows module increases our payment cycle security, and our team has also managed to cut down the time for preparing payments reports from half a day to half an hour.”

“Trustmi provided transparency into our payment process to see where cyberattacks and errors were happening and full protection without changing our workflow."

“Like many businesses today, we’ve experienced cyber attacks on our payment process, but we didn’t realize the extent to which we were at risk until we evaluated Trustmi. Now we’re confident we’ll be able to avoid future attacks with their platform.”

“Trustmi’s platform is an important tool for our team. Their Payment Flows module increases our payment cycle security, and our team has also managed to cut down the time for preparing payments reports from half a day to half an hour.”

$240 Billion Secured

Protecting businesses globally against socially engineered fraud and errors.

Up to 2.5% of Budget Saved

By Eliminating Fraud and Payment Errors

From Hours to Seconds

Manual Process Time Reduced

Behavioral AI-powered security

Behavioral AI-powered security  Protection on day one

Protection on day one  10-15x ROI

10-15x ROI