Fake invoices rarely look fake—which makes them tough to spot.

And it’s happening more often than most teams realize. In our analysis of 260 real-life payment fraud attacks, 39% involved fraudulent financial documents—almost always invoices.

That challenge is only getting harder, as attackers these days use AI to generate highly convincing invoices that eerily resemble real vendor documents. Fraudulent invoices include familiar formatting, expected details, and supporting information that allows them to pass routine checks without raising concern.

Sometimes the only thing that’s wrong is the metadata, which the human eye can’t spot. This is why invoice fraud has become one of the most costly payment threats facing finance teams, with organizations losing more than $1M per year on average.

This guide explains how to identify fake invoices in real-world AP workflows, the red flags that matter most, and the practical strategies organizations use to reduce B2B payment fraud risk.

What Are Fake Invoices?

Fake invoices are fraudulent billing requests designed to trigger unauthorized payments. They are one of the most common forms of invoice fraud, particularly within accounts payable workflows.

In practice, these invoices typically follow a few common patterns:

- Impersonated Vendors: Fraudsters pretend to be a legitimate supplier by copying email addresses or using stolen invoice templates. They send updated payment instructions or new invoices that appear legitimate.

- Duplicate or Altered Invoices: A real invoice is copied or changed, with modifications such as altered amounts, due dates, or account numbers. These often slip through when AP teams are under pressure.

- Overbilling or False Services: Invoices may include inflated quantities, inflated rates, or charges for services or products that were never delivered. These can come from both external fraudsters and dishonest insiders.

- Fake “New Vendor” Accounts: Criminals create fake suppliers, submit convincing documents, and attempt to get approved in your system. This often happens when due diligence is rushed or done manually.

These examples are not exhaustive. If you want a deeper breakdown of invoice fraud types and how they enter payment workflows, see our guide on What is invoice fraud? How it Works and Why it Still Succeeds.

What matters most for detection is not the category. It’s that these invoices are designed to look legitimate and move through routine workflows without immediate suspicion.

Why Traditional AP Controls Miss Fake Invoices

At this point, most finance leaders will say: We already have controls for this.

On paper, those controls look solid. And yet invoice fraud continues to slip through. The issue isn’t that these controls are ineffective. It’s that they were designed to validate documentation, not to identify fake invoices within legitimate workflows.

This gap is reflected in how attacks are designed. In 39% of cases, attackers include fabricated financial artifacts—such as invoices, W-9s, and bank documents—not to bypass controls, but to pass them. They provide justification, making fraudulent requests appear complete and ready for approval.

That distinction is subtle but important.

Many organizations rely on 3-way matching, approval workflows, and ERP controls to catch fraud. But these controls confirm that a transaction appears consistent. They don’t surface when something is slightly off.

Here’s where that gap shows up:

- 3-way matching validates documentation, not authenticity. If a fraudster controls both the invoice and the communication channel, documents can appear aligned while still being fraudulent.

- Email security tools lack payment context. They evaluate message risk but don’t correlate changes in vendor payment behavior. In fact, 85% of payment fraud attacks begin in email and go undetected.

- Bank validation checks format, not ownership. A valid bank account can still belong to a criminal. In over 90% of cases, the bank account itself passes validation checks because the details are real.

- Approval chains assume legitimacy. Approvers confirm business logic, not vendor identity shifts.

When it comes to fake invoices, the documentation is meant to validate that a request is legitimate. These materials don’t raise red flags—they reduce them.

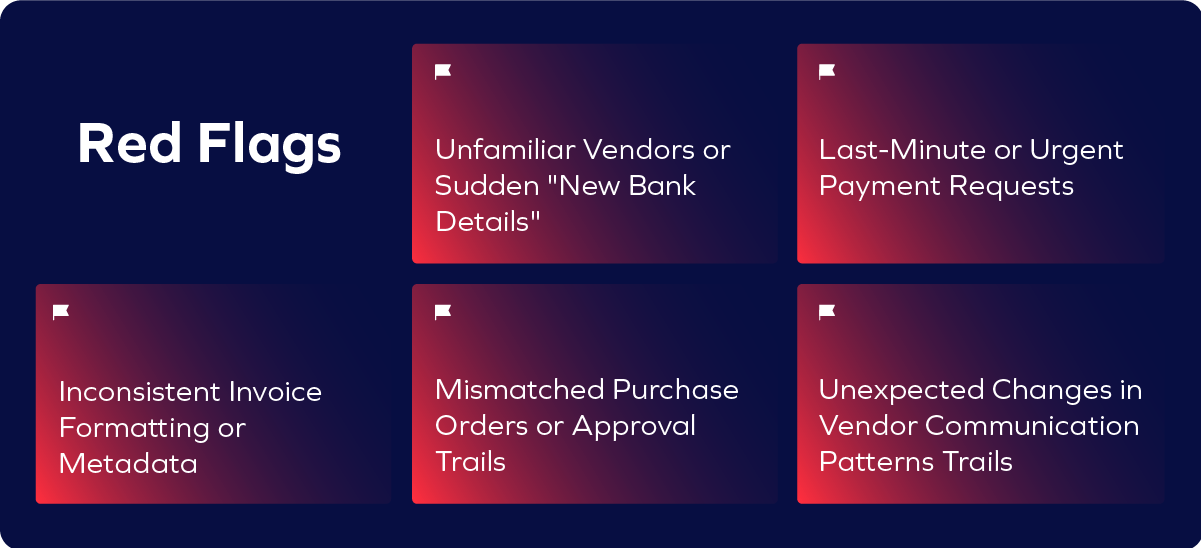

Warning Signs of Fake Invoices

The challenge isn’t that warning signs don’t exist. It’s that they are subtle and often don’t stand out on their own. So when your AP team is reviewing large volumes of invoices, small inconsistencies are easy to miss—especially when each step in the process appears valid.

The following are common indicators of fake invoices. Individually, they may seem minor. Together, they can signal manipulation within an otherwise legitimate workflow.

Spotting these signals manually is difficult, especially in high-volume environments. Invoice validation software can capture risks that humans miss, especially in high-volume AP environments. Modern payment security tools use AI and cross-system analysis to analyze patterns across invoices, vendors, and communication in real time, surfacing inconsistencies that would be difficult to detect through manual review alone.

5 Best Practices to Identify Fake Invoices

If invoice fraud succeeds by looking legitimate across systems, here’s what AP teams should examine before payment.

1. Use Behavioral AI to Detect Anomalies

Some AP teams may still try to manually spot unusual payment patterns, but without integrated systems, detecting these anomalies is a reactive process and often relies on historical payment data, which is prone to gaps and errors.

This is why behavioral AI is critical to identify fake invoices. By continuously tracking how vendor and payment activity evolves over time, organizations can detect deviations as they happen, not after the fact. Patterns that would be missed in a single transaction become visible when viewed in context.

These tools use AI to recognize behavioral shifts, like a spike in vendor payments or new vendor bank accounts, enabling teams to catch fraud before it’s processed. This allows teams to move beyond reviewing individual invoices and instead detect when something doesn’t align with how payments normally behave.

2. Analyze Email in the Context of Payments

Fraudulent emails can look extremely convincing, especially when bad actors use sophisticated tactics, such as executive impersonations. In large organizations, email security tools may not always flag fraud due to the lack of financial context or visibility into the payment workflow.

The issue is not just whether an email is malicious. It’s whether it makes sense in the context of a payment request.

A comprehensive email monitoring solution that integrates with payment systems can help detect fraud early. By analyzing both the context and authenticity of emails in relation to payments, teams can identify social engineering attempts before invoices are approved.

3. Detect Hidden Invoice Manipulation and Metadata Changes

In large companies, metadata review (e.g., creation dates, author information) is usually only done if fraud is suspected. Many teams overlook this step due to the sheer volume of invoices that need to be processed.

Fraudsters can easily manipulate invoices without making them look obviously wrong. Instead of creating fake invoices from scratch, they often modify real ones—changing key details in ways that blend into normal workflows.

This can include:

- Bank account information altered after initial submission

- Invoice amounts or line items modified post-approval

- Document metadata showing recent edits or unexpected authors

- File creation timestamps that don’t align with invoice dates

- Unknown editing software or suspicious file conversion history

On the surface, the invoice still looks correct, and that’s why these changes get missed.

Enterprises need an automated way to monitor document integrity in real time. Without it, detecting hidden edits or tampered metadata becomes nearly impossible at scale. This means checking not just the invoice itself, but the history behind it, before it’s approved for payment.

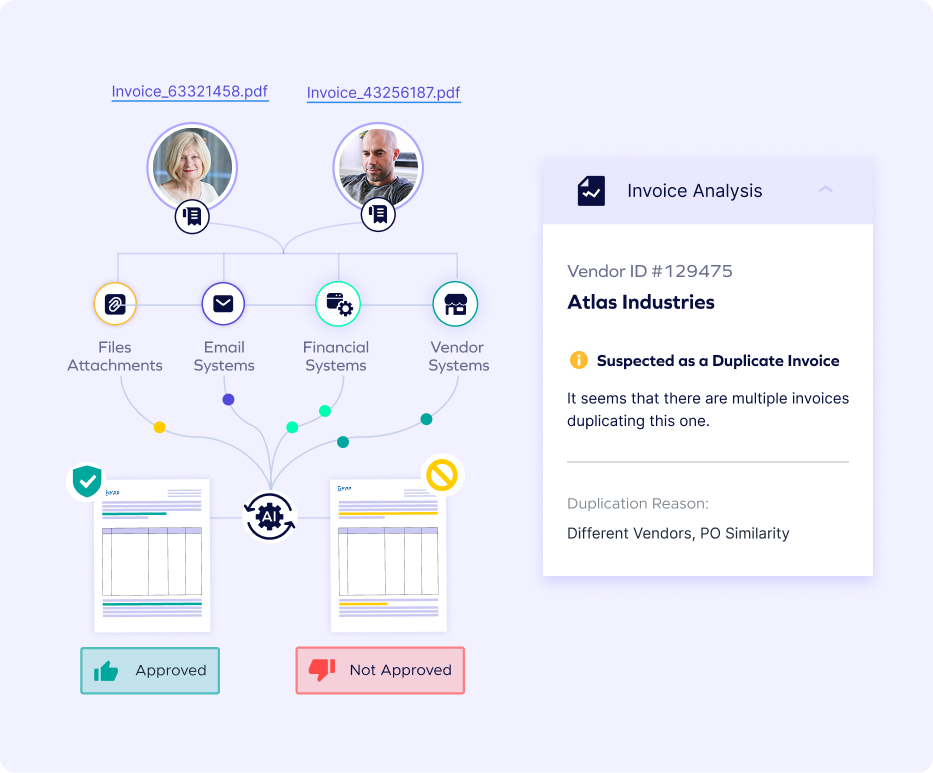

4. Connect Signals Across Systems

In most organizations, different parts of the invoice process live in different places: email, ERP systems, vendor records, approval workflows.

Each one gets checked. And each one looks fine. That’s the problem. Fraud today isn’t obvious. It’s designed to look legitimate at every step.

For example:

- The email looks like it came from a real vendor—but it didn’t

- The invoice matches the purchase order—but something about it is off

- The bank details look valid—but they’re not the ones you’ve used before

- The request moves through approvals without raising any flags—but it shouldn’t

If you look at any one of these on its own, it may not raise enough concern to stop a payment. But when you look at them together, the story changes. That’s where fraud becomes visible.

Many organizations already automate parts of this process—like vendor verification or PO matching—to move faster. But when those checks happen in isolation, they can still approve fraudulent transactions that look legitimate on their own.

The difference is using a system that brings this data together: comparing invoice details against vendor records, purchase orders, and historical activity across systems. It helps spot what doesn’t add up before the payment is approved.

This is exactly how platforms like Trustmi detect fraud: connecting signals across the entire payment workflow, instead of relying on isolated checks.

5. Train Staff to Recognize Social Engineering Tactics

Humans also need to be part of the solution too. It’s crucial to regularly train employees on social engineering tactics, but that doesn’t mean generic security awareness training is enough.

Accounts payable teams are a primary target for invoice fraud, and the attacks they face are different.They don’t just receive phishing emails, they receive realistic invoices, vendor requests, and payment changes that appear to follow normal business processes. That’s why AP teams need training that reflects how fraud actually shows up in their day-to-day workflow.

This includes:

- Recognizing suspicious payment changes, even when they appear legitimate

- Identifying unusual vendor behavior or requests

- Understanding how fraud can move through normal approval processes

While training is essential, it should be complemented by systems that reduce reliance on manual judgment.

Because the reality is: these attacks are designed to look normal, even to experienced teams.

How to Identify Fake Invoices Before Payments Are Approved

Fake invoice fraud is harder to spot and more damaging to organizations of all sizes. From impersonated vendors to manipulated invoices and fake onboarding requests, the threats are real, and relying solely on manual checks is no longer enough.

The best defense is a combination of trained people, disciplined AP processes, and intelligent technology that closes the gaps humans can’t always see.

The organizations that catch these attacks aren’t checking more—they’re connecting more.

That’s the shift modern finance teams are making. They’re moving from isolated checks to connected, context-aware detection. Platforms like Trustmi are built around this approach of helping organizations detect fraud in real time by analyzing invoices, vendors, payments, and communication together.

If you want to see how this works in practice, explore how invoice validation software can help you detect fraud before payments are approved, or book a demo to see how Trustmi applies this approach in real workflows.

Behavioral AI-powered security

Behavioral AI-powered security  Protection on day one

Protection on day one  10-15x ROI

10-15x ROI