Many organizations believe their payment systems are secure because they have a strong bank account verification. While this is an understandable assumption, it is also the exact assumption modern fraudsters are counting on.

Here is the uncomfortable reality: 90% of B2B payment fraud accounts are bank-approved. The account checks out, the name matches, routing number are correct, and the money still lands in a fraudster’s account.

Validation did not fail in these cases. It worked exactly as designed, and that is the problem. Account validation is built to confirm that information is accurate. But fraud no longer hinges on submitting inaccurate information. Modern attackers have mapped out the payment process from end to end. They understand which checks are run, what triggers a flag, and how to build a request that passes cleanly through every check.

In this post, we will cover what bank account validation actually does, why it fails against modern payment fraud, and what an effective fraud-prevention approach looks like for B2B payments.

What Is Bank Account Validation and How Does It Work?

To understand why validation falls short, it helps to be clear about what it actually does and how it differs from basic verification.

Bank account verification confirms that an account exists. It checks the account number and routing number to make sure they are real and active. This is the baseline check, and some businesses stop here and proceed with payments as soon as they know the account exists.

Bank account validation, on the other hand, goes a little bit further. It cross-checks the account holder’s name, address, and other identifying information. The goal is not just to confirm that the account exists, but that it belongs to the entity you expect to be paying. For organizations running on verification only, moving to full validation is a meaningful upgrade. It catches mismatches between vendor details and bank records, flagging basic fraud attempts and clerical errors alike.

The only gap is that validation is designed to check correctness. What it cannot check is context—and that is exactly where sophisticated fraud lives.

The BEC Playbook: How Attackers Design Around Bank Validation

Business email compromise (BEC) attacks are the clearest illustration of how fraud is specifically engineered to pass validation.

An attacker begins by compromising the email account of someone on a vendor’s finance team. With inbox access, they can read invoices, payment histories, client contact lists, and banking correspondence. They understand the relationship between the vendor and its clients better than most people on either side do.

Armed with this intelligence, the attacker opens a new bank account using the vendor’s real details—often at the same bank the vendor already uses. The account is legitimate. The information is accurate. The bank has no reason to flag it.

From there, the attacker impersonates the vendor, submits invoices, and requests an update to the bank account on file. When the client’s finance team runs validation on the new account, it passes. Why? Because the name matches, the routing number is correct, and everything checks out.

What makes this effective is that the fraudster does not need to deceive the validation system. They just need to satisfy it. The fraudster’s account can also be opened at a completely different bank and still go undetected because no central database links accounts across institutions. Fraudsters are increasingly targeting third-party vendor relationships because they know that is where the payment process is most exposed.

Why Bank Account Validation Cannot Prevent Modern Payment Fraud

Bank account validation only confirms that an account is real. It can’t confirm who actually controls it. So, when a payment fraud occurs, everything is in order from the system’s perspective.

Validation has no visibility into what happened before those account details arrived in your inbox.

- It won’t tell you whether a banking change request came through a compromised email channel.

- It won’t notify you whether the vendor has any awareness of the request being made in their name.

- It also won’t tell you whether the vendor changed these details for everyone—or just for you.

These are trust and context problems, and they are exactly where sophisticated fraud lives.

The problem is not that validation fails. The problem is that validation was never designed to detect modern B2B payment fraud.

What Effective Payment Fraud Prevention Actually Requires

Closing the gap that validation leaves open requires a different kind of approach. You need to think about where fraud enters the payment process and what it would take to detect it there.

A complete approach needs to address five things:

1. Validate Changes in a Closed Loop

You already know this one, and there’s a good chance your organization is already doing it. When a vendor requests an account change, that request needs to be confirmed directly with the vendor.

When a vendor requests an account change, that request should be confirmed directly with the vendor through a channel completely independent of the original request. Call-back verification procedures, for example, help close the window fraudsters rely on when initiating changes through compromised inboxes.

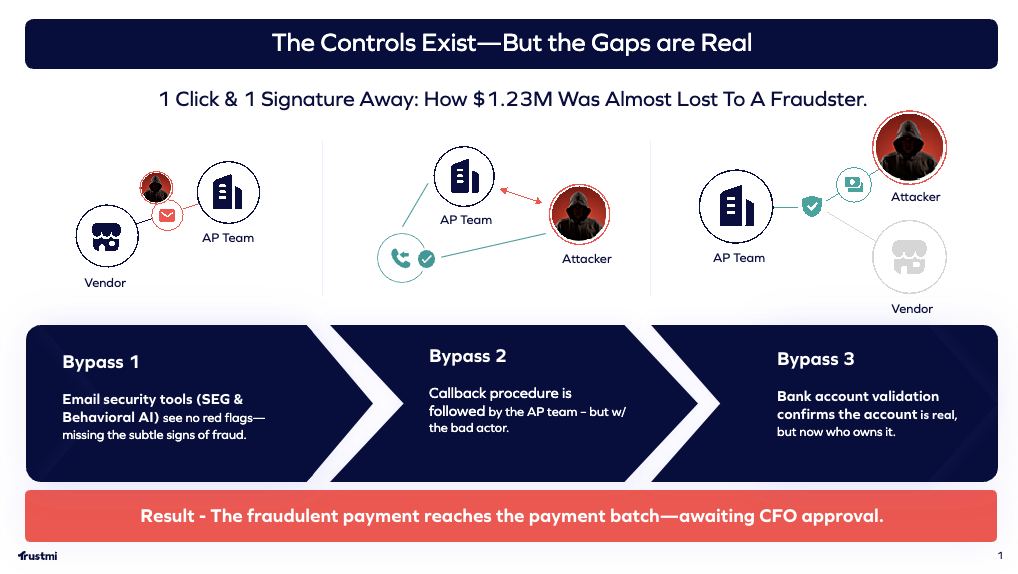

Warning: The Limitations of Vendor Call-Backs

This step absolutely matters. It helps stop basic fraud attempts and remains an important control. But modern payment fraud increasingly exploits the limitations of this process itself.

As we’ve seen in real-world attacks, organizations often believe they verified the vendor when in reality, they verified information already controlled by the attacker. A fraudster compromises a vendor’s email account and submits a payment change request. Along with it, they provide “updated” contact information for verification. When the finance team performs the callback, they end up speaking directly to the attacker—who confidently confirms the request while posing as the trusted vendor.

We’ve seen this tactic again and again, and you can read about a real example of this that almost cost a company $1.23M. And increasingly, voice deepfakes introduce yet another way to undermine the reliability of traditional call-back procedures.

2. Control the Source of Vendor Change

Any process that allows vendor banking details to be updated through email is exposed. Email is the most compromised channel in B2B finance. In the recent Trustmi Benchmark Report, it found that 85% of payment fraud attacks start in email—and bypass email security. And it is where most account-change fraud originates.

A more secure approach requires vendors to manage banking details through a controlled, verified environment rather than through open communication channels attackers can hijack. The challenge is that traditional email security platforms were not built to understand financial intent or payment workflow risk. They stop at the inbox.

That is why many leading email security providers are partnering with end-to-end payment fraud prevention platforms that extend protection beyond the inbox and into finance operations. As Mimecast explained in its partnership with Trustmi, the integration helps, “extend email and BEC protection into financial workflows where real damage can occur.”

3. Analyze Behavior Across the Full Payment Process

Fraud is not always visible in the account details. More often, it appears in the behavior surrounding the request.

- An invoice suddenly arrives at an unusual time.

- A vendor who normally communicates with AP directly starts copying executives.

- A payment request creates urgency that feels slightly out of character.

- A trusted vendor changes both banking details and contact information within days of each other.

Individually, none of these signals may seem suspicious enough to stop a payment. Together, they often reveal that something is wrong. That is the challenge with modern payment fraud: the attack is rarely isolated to a single field or validation step. It unfolds across emails, invoices, workflows, timing, and communication patterns.

The recent Trustmi Benchmark Report reinforces this shift, finding that 59% of payment fraud attacks deployed two or more coordinated tactics. The challenge is that no single signal looks fraudulent on its own. The risk only becomes visible when these signals are analyzed together.

Identifying these patterns consistently requires systems capable of continuously analyzing behavior across communication channels, vendors, invoices, and payment workflows in real time.

4. Re-Verify Continuously

Vendor details that were legitimate at onboarding can become a liability later. A relationship that looked clean six months ago may have since been compromised through email takeover, credential theft, or changes inside the vendor organization itself.

A one-time validation check is not a permanent seal of trust.

Attackers increasingly take advantage of long-standing vendor relationships because they carry less scrutiny and more institutional trust. The benchmark report found that of 250 real-world B2B payment fraud attacks observed, 92% used the authority of an executive, vendor, or both in their attack. Ongoing monitoring means that when something about a vendor’s profile shifts, banking details, communication patterns, contact information, payment timing, or workflow behavior, it gets caught before money moves.

5. Introduce Cross-Organization Visibility

One of the most powerful fraud signals is isolation. If a vendor is genuinely updating their banking details, that update tends to be consistent across their business relationships. If a change request appears for only one client, with no corresponding activity anywhere else, that is a strong signal that something is wrong. Detecting these inconsistencies requires network-level intelligence across organizations—a capability that only purpose-built security payment platforms can realistically provide at scale.

Platforms like Trustmi are built around this model, layering these capabilities onto existing payment workflows to close the gaps that validation alone leaves open.

The Industry is Moving in This Direction

If you’ve been following NACHA’s upcoming 2026 ACH fraud prevention requirements, some of these recommendations may sound familiar.

That is not a coincidence.

Industry bodies like Nacha are increasingly recognizing the growing limitations of traditional finance and security controls in stopping modern payment fraud. The direction is clear: Organizations can no longer rely solely on static validation checks or point-in-time verification processes. Effective fraud prevention increasingly requires continuous monitoring, behavioral analysis, stronger payment verification controls, and broader visibility into payment risk.

In other words, the industry is moving toward a more contextual and continuous approach to payment security—one designed to address how modern fraud actually operates.

For organizations trying to better understand the upcoming NACHA requirements and what they mean operationally, we break down the changes in more detail here:

- Nacha’s 2026 Rule Changes: What Finance Teams Must Do—And What’s at Risk

- How to Meet Nacha 2026 Requirements and Why Trustmi Is Built for It

Modern Fraud Is Designed to Pass Your Controls

A major problem with relying on bank account validation is that fraud has been deliberately designed to satisfy it. Attackers research payment workflows before they act. They know which controls are in place, and they build their approach around passing them cleanly.

Catching that requires more than a confirmation that an account is real. It requires visibility into the trust signals surrounding every payment request: the behavior, the communication patterns, and the broader network signals that validation alone was never built to see.

For a deeper look at how modern payment fraud gets approved and what the data from real-world attacks reveals about where controls are falling short, the Trustmi Payment Security & Risk Benchmark Report is the right starting point. You can also explore exactly how attackers exploit bank validation gaps in the Behind the Breach webinar series.

Behavioral AI-powered security

Behavioral AI-powered security  Protection on day one

Protection on day one  10-15x ROI

10-15x ROI