Nacha’s 2026 rules changed the ACH fraud conversation. The question is no longer whether fraud monitoring needs to improve. It is how to meet the new requirements in a way that meaningfully reduces risk.

That is where solution choice becomes critical. Some platforms focus on account validation. Others streamline documentation. Far fewer give teams a complete view of payment risk across vendors, systems, and workflows to help stop sophisticated fraud before money moves.

While compliance may be the immediate driver, many organizations are using this moment to modernize controls, reduce manual work, and address payment fraud exposure that existed long before the deadline.

This guide explains what capabilities matter, how to compare solutions, and what to prioritize when choosing an approach that meets Nacha requirements.

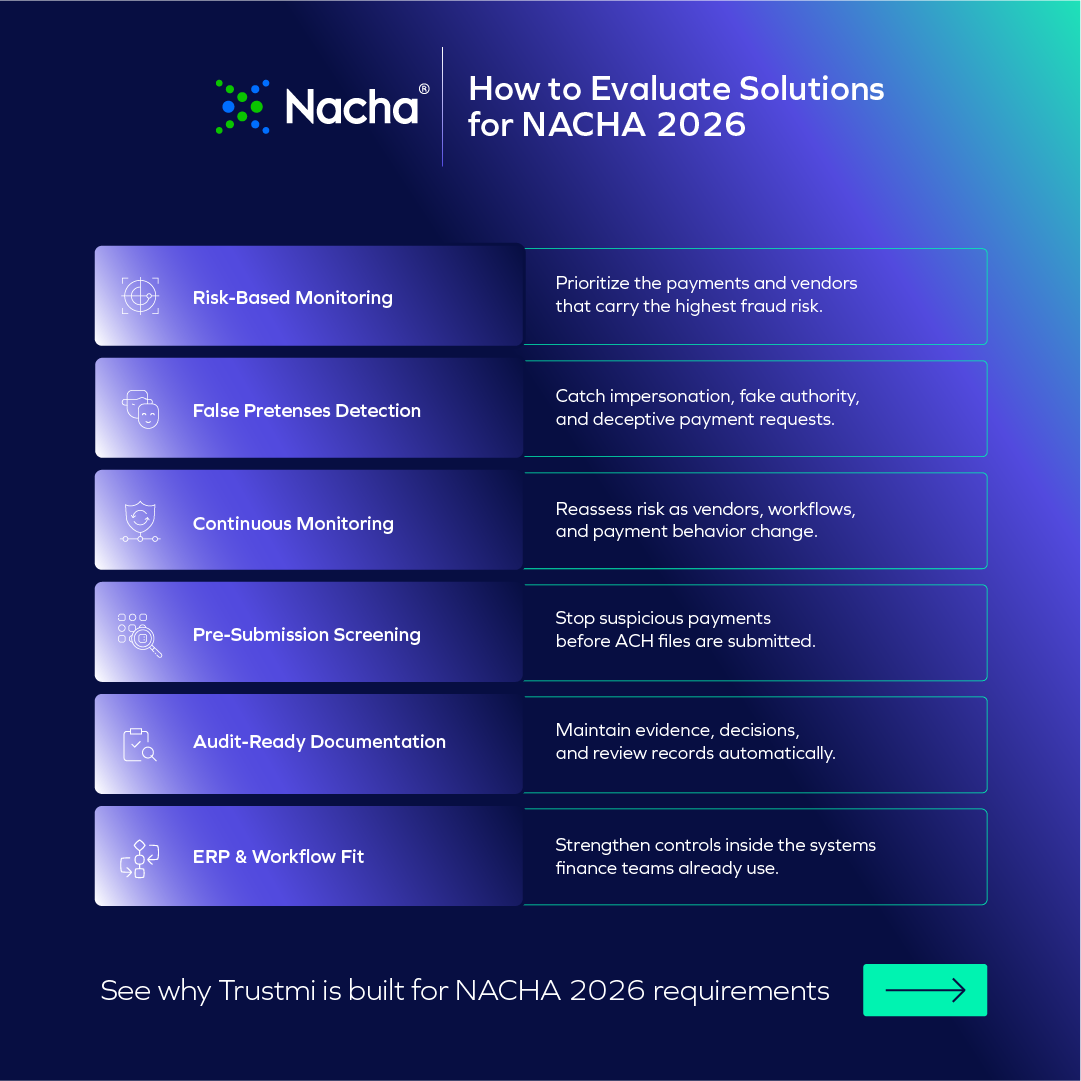

Must-Have Capabilities to Meet Nacha’s New Requirements

Nacha’s 2026 updates introduce specific expectations around fraud monitoring, risk management, and ongoing oversight. When evaluating vendors, these are the core capabilities that should be clearly addressed.

Risk-Based Monitoring

Nacha expects organizations to apply greater scrutiny where risk is higher rather than treating every payment the same way.

Prioritize capabilities such as:

- transaction risk scoring and prioritization

- behavioral baselines for vendors and payments

- detection of unusual activity

False Pretenses Detection

Nacha now explicitly calls out False Pretenses fraud, including misrepresentation of identity, authority, or account ownership.

Strong solutions should include:

- impersonation and suspicious request detection

- contextual risk analysis beyond data matching

Continuous Monitoring

Fraud risk does not end after onboarding or a one-time review. Nacha’s direction is toward ongoing oversight as conditions change over time.

Look for support for:

- continuous monitoring of transactions and workflows

- alerts for vendor or process changes

- ongoing risk reassessment

Pre-Submission Screening

The strongest control point is before money enters the ACH network. Nacha emphasizes identifying suspicious activity before submission.

Evaluate whether the platform provides:

- real-time payment screening before release

- clear escalation or hold mechanisms for high-risk transactions

Audit-Ready Documentation

Organizations must be able to demonstrate how fraud monitoring works, what actions were taken, and how controls are reviewed over time.

Look for capabilities such as:

- logged decisions, actions, and timestamps

- centralized audit trail with supporting evidence

What to Look for in a Solution

The capabilities above are a good starting point, but not every solution that checks those boxes delivers in practice. Also, meeting the requirement is the baseline. The bigger question is whether your approach can actually reduce the fraud that traditional controls still miss—while lowering manual work and improving how payment decisions are made.

To make sure you’re choosing a solution that truly delivers on compliance—and goes beyond it—here are a few key things to look for:

Detects False Pretenses, Not Just Bad Data

Don’t confuse detection of bad data with detection of false pretenses. Legacy tools are often built to catch bad data: mismatched account details, incomplete records, or formatting errors. But False Pretenses bypasses that logic because the request itself may appear perfectly legitimate.

What matters is context. Does the request align with established vendor behavior? Is the timing unusual? Were recent changes made just before the request arrived? Do surrounding signals suggest elevated risk? The issue is no longer whether the information is accurate. It is whether the request deserves trust.

Ask: Does this solution truly detect sophisticated false pretenses that bypass traditional controls?

Protects the Full Process, Not Just the Payment File

You can’t rely on single-point verification. Fraud rarely begins at the moment of payment release. Yet many controls activate only when a payment file is created or submitted, long after risk may have entered the process.

Compromise often starts earlier through vendor onboarding, bank account changes, invoice activity, approval workflows, or payment creation. By the time funds are ready to move, the warning signs may already be buried upstream. Effective protection extends across the payment lifecycle rather than concentrating only on the final transaction.

Ask: Does this solution provide continuous, end-to-end protection across the payment process?

Sees the Full Picture, Not Just One System

Coverage across the workflow still falls short if signals remain trapped in separate systems. Modern fraud is often subtle in any one place and obvious only when multiple indicators are viewed together.

A routine-looking email. A quietly edited vendor record. An invoice arriving slightly outside the usual cycle. Payment behavior that drifts from historical patterns. Each event may seem harmless in isolation. Combined, they can point to meaningful risk. That is why connected visibility matters more than isolated controls.

Ask: Does this solution integrate signals across systems and provide intelligent analysis, or just collect data in one place?

Gives Teams Answers, Not More Alerts

Alert volume is not the same as protection. When systems generate constant notifications without clear context, response slows and teams spend time triaging noise instead of addressing real threats.

Better platforms prioritize what matters most and translate complexity into clear action: proceed, stop, or review. That clarity helps finance and treasury teams move faster, align more easily, and make decisions with confidence.

Ask: Does this solution give clear, actionable guidance on what to do with risky payments?

Automated Documentation, Not More Manual Work

For many organizations, the evidence needed for annual reviews is scattered across email, ERP systems, payment platforms, shared drives, and internal notes. When review season arrives, teams are forced to reconstruct decisions after the fact.

Well-designed platforms capture that record continuously—preserving decisions, supporting signals, reviewer actions, timestamps, and evidence as part of normal operations rather than as a separate compliance exercise.

Ask: Does this solution consolidate documentation so reviews are fast and straightforward?

Implementation and Adoption Considerations

Capabilities matter, but even strong controls can fail if they are difficult to deploy or too burdensome for finance teams to use consistently.

Works With the ERP and Payment Systems You Already Use

Finance teams already run critical payment workflows inside ERP systems and connected payment platforms. Fraud controls should strengthen those processes, not force teams into separate tools or manual workarounds.

Look for solutions that integrate directly with your ERP, payment platforms, and approval flows so teams can review risk and act without leaving the systems they already use. The easier it fits into existing workflows, the more likely it is to be adopted.

Reduces Manual Review Instead of Adding More Work

Many organizations already rely on callbacks, spreadsheet checks, approval chasing, and one-off investigations to manage payment risk. A new solution should reduce that burden, not add another queue to manage.

Look for automation that helps teams focus only on the highest-risk activity while allowing low-risk payments to move efficiently. The best platforms improve control while giving time back to AP, treasury, and finance teams.

Fast Time to Value Before the Deadline

Nacha deadlines are fixed, but long implementation cycles don’t have to be. Finance teams shouldn’t need a lengthy IT project or major process redesign to improve controls.

Speed matters. Clear implementation plans, minimal internal lift, and fast integration with core systems determine whether a solution delivers value quickly or becomes another delayed project.

Built for Finance, Not Just Technical Users

Even the most advanced platform will fall short if finance teams don’t use it consistently.

Adoption depends on usability. Clear decisions, intuitive workflows, and minimal training make it easier for AP and treasury teams to incorporate controls into daily operations. The best solutions are powerful enough to reduce risk and simple enough to use every day.

Why Trustmi Is Built for This

Taken together, these requirements highlight a larger reality: organizations need more than point solutions or manual controls. They need a platform built for how payment fraud actually works today.

Trustmi was designed from the ground up for B2B payment fraud, specifically the social engineering and impersonation attacks that Nacha’s 2026 rules are written to address. Here is how it maps to what the requirements demand:

Behavioral AI Instead of Static Rules

Rather than static rules, Trustmi builds vendor-specific behavioral baselines for every vendor and counterparty. Each relationship accumulates a Trust Score reflecting its established patterns. The system then evaluates every payment instruction against that history. So a banking update from a vendor with a three-year track record can look different from the same update from a vendor added last month.

SAFE / UNSAFE Decisions Before Payment

Every payment receives an automated verdict before execution.

- Safe

- Unsafe

- Review Required

That helps AP, treasury, and finance teams act quickly without sorting through endless alerts or ambiguous risk signals.

Audit Readiness by Default

Every decision including, the risk signals evaluated, the Trust Score, and the outcome is logged. When the time for annual review comes, the documentation is structured and ready. Because of how we approach fraud, audit readiness is built in.

Native ERP and Payment Integrations

Trustmi connects with the ERP, email, and payment platforms finance teams already use. Implementation does not require a long IT project or major process redesign. Teams can strengthen controls inside existing workflows and realize value faster.

This makes Trustmi uniquely suited to help organizations meet Nacha requirements while modernizing fraud prevention.

Meet Nacha Requirements With Stronger Payment Protection

As Nachas 2026 rules take effect, compliance is only part of the equation. The bigger question is whether your current approach can actually keep up with how fraud is evolving.

The right solution should help you move beyond fragmented checks and manual reviews. It should give your team clear risk signals, enable faster and more confident decisions, and create a natural audit trail as part of everyday workflows. It should also reduce the noise. Not every payment needs scrutiny—but the ones that do should be impossible to miss.

And most importantly, it should help you identify deception before money moves, not after.

Ready to see how all this works? Book a demo or request a free Nacha readiness assessment.

Behavioral AI-powered security

Behavioral AI-powered security  Protection on day one

Protection on day one  10-15x ROI

10-15x ROI